To examine how China’s semiconductor industrial policies are reshaping the global supply chain, the DSET Economic Security Research Program’s non-resident fellow Mervyn Ho Ming-yen (PhD student in Business & Public Policy, University of California, Berkeley) has released a new research report, Let a Hundred Flowers Blossom: Local Competition and the Rise of Chinese Semiconductor Capacity. Drawing on extensive longitudinal data on wafer output, official subsidies, and government equity participation across Chinese semiconductor firms, the report analyzes the rapid build-out of China’s semiconductor manufacturing capacity and the pathways through which Chinese players are gaining ground in international markets.

China’s Semiconductor Industrial Policy: A “Hundred Flowers” Pattern of Decentralized Institutions

Following the earlier DSET Economic Security Research Program study, The Great Siege: The PRC’s Comprehensive Strategy to Dominate Foundational Chips, this new report again offers a structured assessment of China’s national semiconductor strategy—this time through the lens of center–local dynamics and decentralized policy incentives.

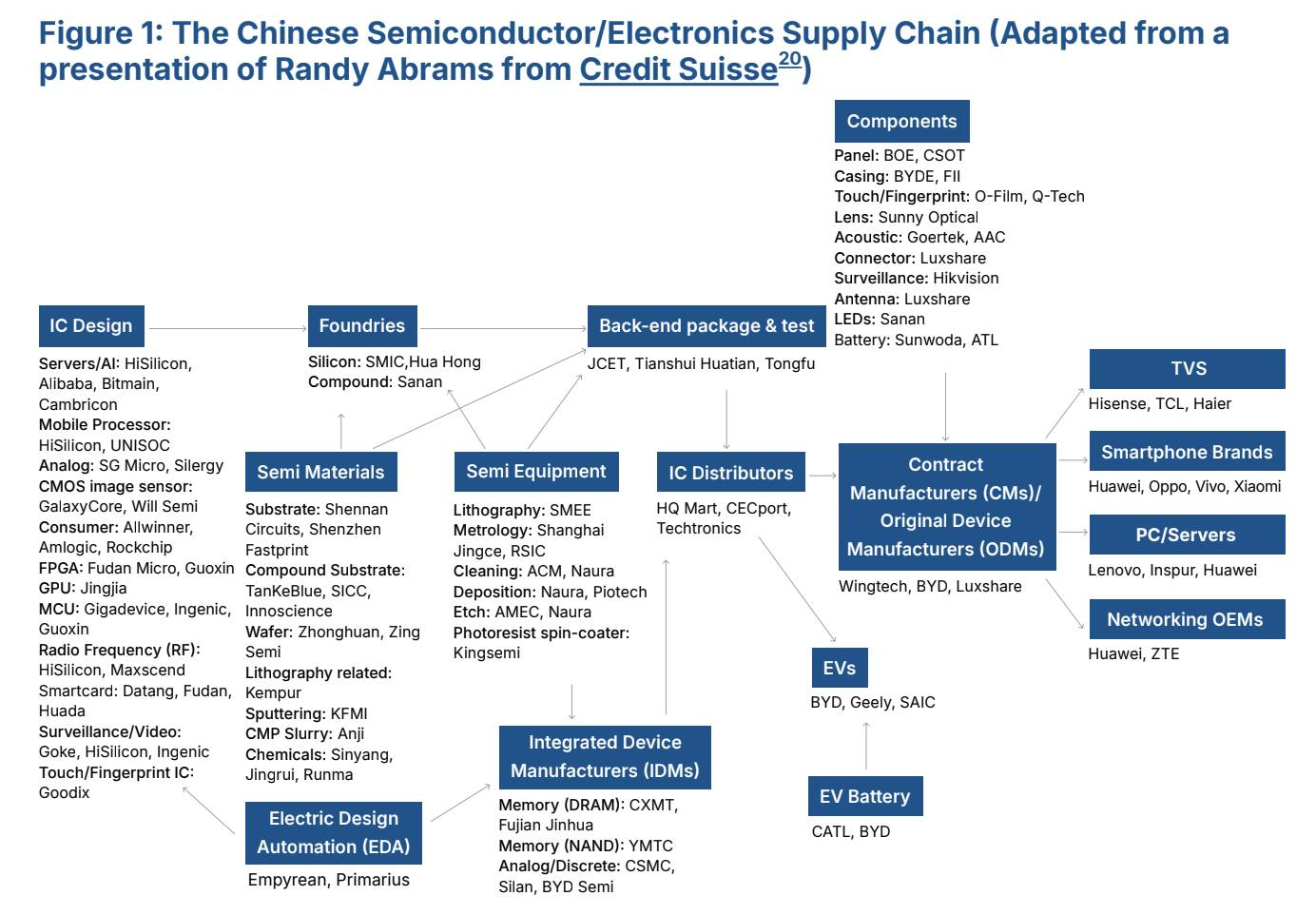

China’s Semiconductor Supply Chain (excerpt from the report)

The report shows how Beijing seeks to coordinate national resources, set unified development goals, and cultivate globally competitive “national champion” firms across each link of the semiconductor supply chain. At the same time, local governments pursue their own vertically integrated, locally controlled ecosystems spanning chip design, manufacturing, and end-market products—each locality intent on surpassing domestic rivals.

In practice, even though state support for the semiconductor sector has reached unprecedented levels nationwide, resources have flowed in a highly fragmented manner across regions, sub-sectors, and firms. This dispersion has produced subsidy misallocation: government support often props up low-productivity firms that would otherwise exit.

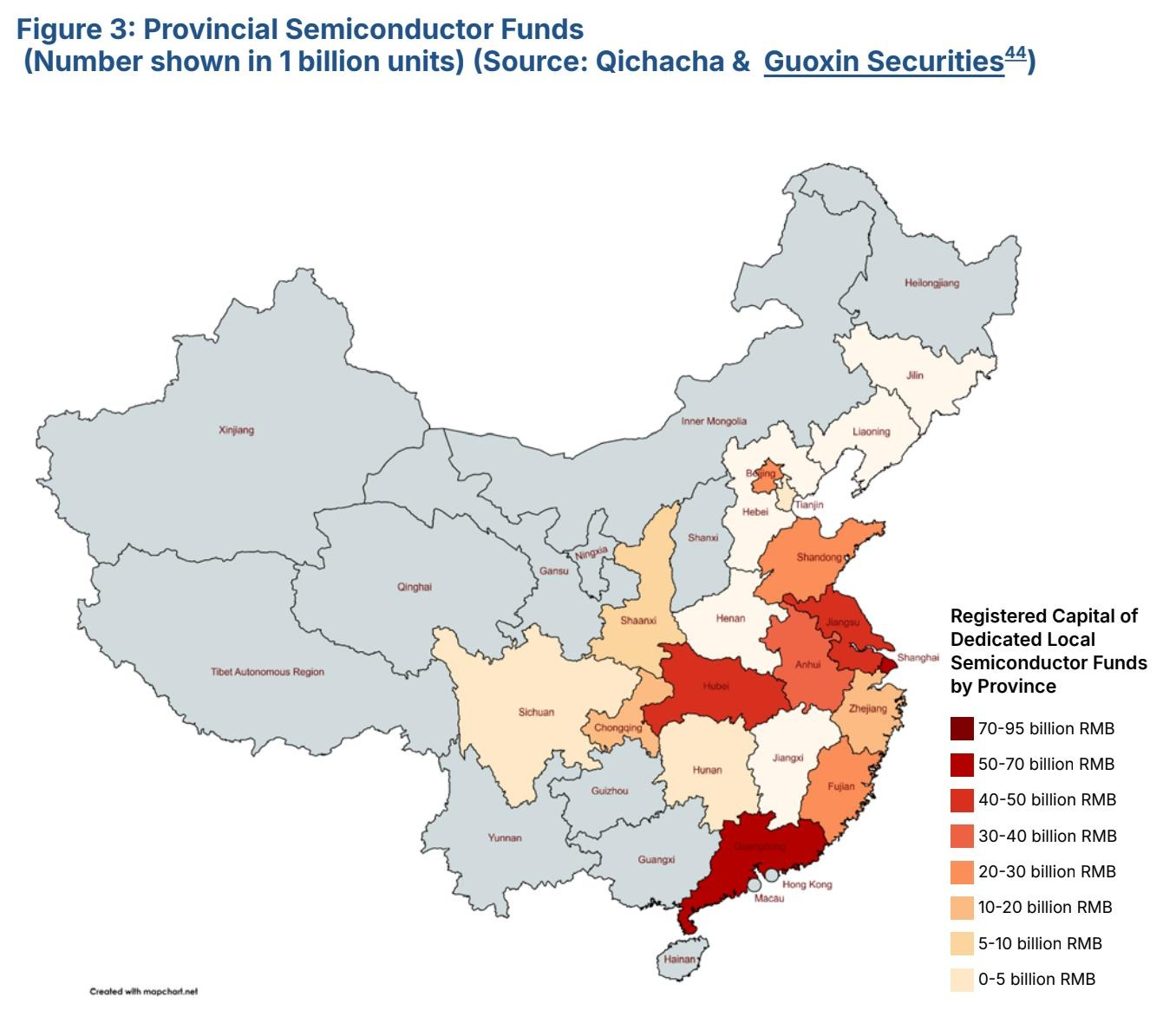

Distribution of Local Semiconductor Funds (excerpt from the report)

Yet the report stresses a countervailing effect: this distinctly Chinese, decentralized policy structure has also preserved competitive market pressures. Because local officials chase production volume, sales, and national market-share targets—frequently with little regard for profitability—numerous high-profile failures have occurred. Nevertheless, efficient firms are rewarded in this environment: competitive pressure drives cost reduction and technological innovation, enabling the most capable producers to scale into global markets and improve their competitive standing.

That same local competition, however, has propelled relentless expansion of Chinese wafer manufacturing capacity, pushing prices downward. Even amid falling prices, firms continue to build and ramp, especially in mature process nodes—often with multiple state-supported producers operating in the very same technology segments. As highlighted in The Great Siege, this dynamic is placing significant competitive pressure—often perceived as unfair—on international suppliers.

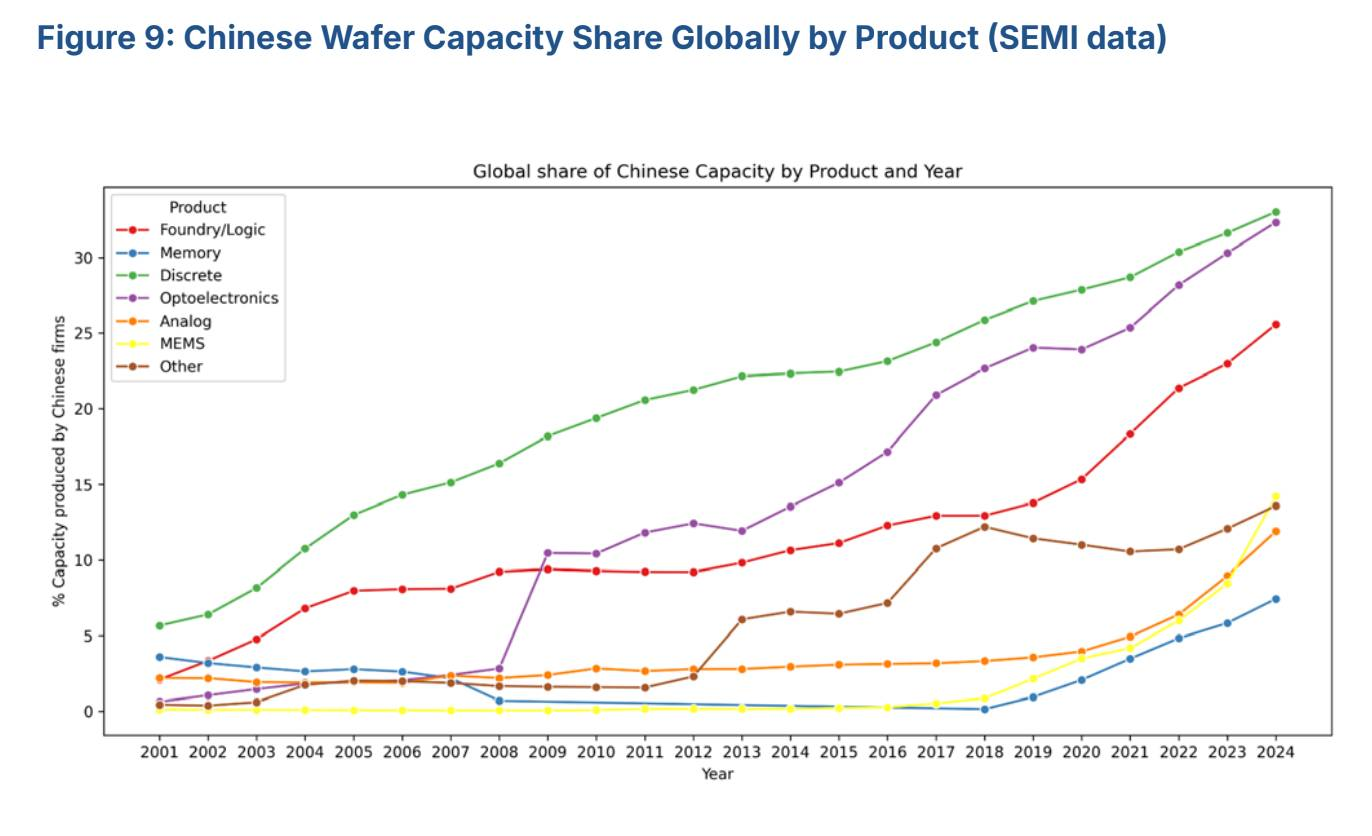

China’s Global Market Share in Wafer Fabrication Capacity (excerpt from the report)

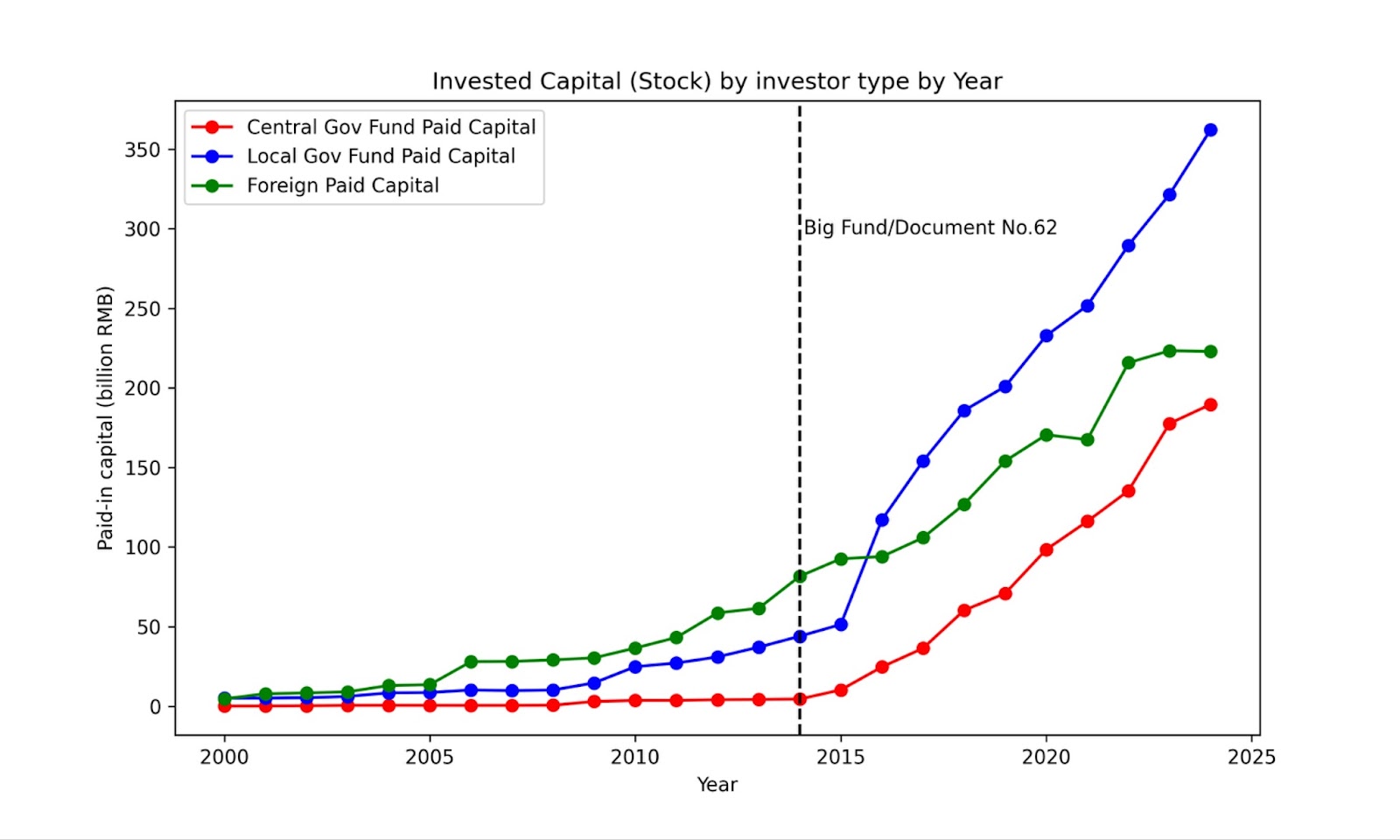

Comparison of Central/Local Government Investment and Foreign Capital in China (excerpt from the report)

Let a Hundred Flowers Blossom argues that the United States, Japan, Europe, and other tech democracies must grasp the decentralized institutional logic underlying China’s semiconductor build-out. It is a mistake to attribute China’s capacity expansion solely to top-down direction from the central state. In reality, capacity is being driven by multiple competing actors: national-level foundry leaders such as SMIC and Huahong, as well as locally backed manufacturers supported by provincial and municipal governments.

From Fragmentation to Re-Centralization: The Next Phase in China’s Semiconductor Policy

From Beijing’s perspective, the current development logic is suboptimal. Fierce inter-local competition makes it difficult to concentrate policy resources on the relatively small number of firms that are genuinely productive and globally competitive. In response, the central government has begun to recalibrate industrial policy:

- Huawei has reportedly been tasked with coordinating a domestically sourced, vertically integrated supply chain composed of multiple state-backed “national champion” firms.

- Phase III of the National Integrated Circuit Industry Investment Fund (“Big Fund”) has sharply curtailed broad local participation, retaining equity contributions only from Beijing, Shanghai, and Guangdong.

- In critical semiconductor equipment and other strategic technology segments, Beijing has launched consolidation efforts aimed at reducing roughly 200 toolmakers nationwide to about 10 core players.

Still, heavy recentralization brings risks. If future semiconductor policy relies too heavily on central decision-making, can Beijing reliably identify winning pathways across such a complex hardware supply chain? Considerable uncertainty remains. One of China’s central challenges going forward will be how to retain the dynamism of local competition and experimentation while moving toward a more centralized industrial regime.

Targeted Controls & Coordinated Agreements: A Collective Response to the “China Problem” in Chips

Overcapacity, price compression, aggressive industrial policy, and contested trade practices have already combined to create what many in global markets call the “China problem” in semiconductors. In confronting China’s Hundred-Flowers-style policy model, this report argues that multilateral coordination among tech democracies should anchor the strategic response. The author advances two main policy recommendations:

1. Targeted Export Control Strategy

In the near to medium term, China’s domestic share in key semiconductor production equipment and materials remains relatively low. Expanding export restrictions by technology-aligned countries on tools and materials used in mature process manufacturing (e.g., 14–65nm class technologies) could materially disrupt China’s ability to scale capacity.

In addition, unilateral U.S. tightening on Electronic Design Automation (EDA) tools can constrain Chinese chip design firms working in the 3–28nm range from partnering with foundries in Taiwan, South Korea, and other Western jurisdictions. That said, the marginal impact of further restrictions is more limited for already sanctioned firms such as Huawei HiSilicon and Cambricon.

2. Multilateral Semiconductor Supply Chain Agreements

Even as the United States investigates unfair trade practices related to Chinese mature-node chips, European integrated device manufacturers (IDMs) continue to expand investments in China and enter into joint ventures or supply agreements with Chinese firms, resulting in a divergence of strategic priorities among democratic economies. To address this policy misalignment, the United States, Europe, Taiwan, South Korea, and other like-minded partners should negotiate multilateral agreements on semiconductor supply chain coordination, which may include:

- Jointly established tariffs and outbound investment restrictions to deter non-market behavior;

- A trusted network for free trade among democratic semiconductor supply chain participants;

- Mechanisms for capacity coordination and collaborative R&D in advanced and specialized process technologies;

- Priority access to secure foundry capacity for strategic sectors such as defense, telecommunications, and aerospace;

- Dedicated policy incentives for application-specific process R&D, enabling mature-node foundries to pursue product differentiation in logic and analog chip markets.